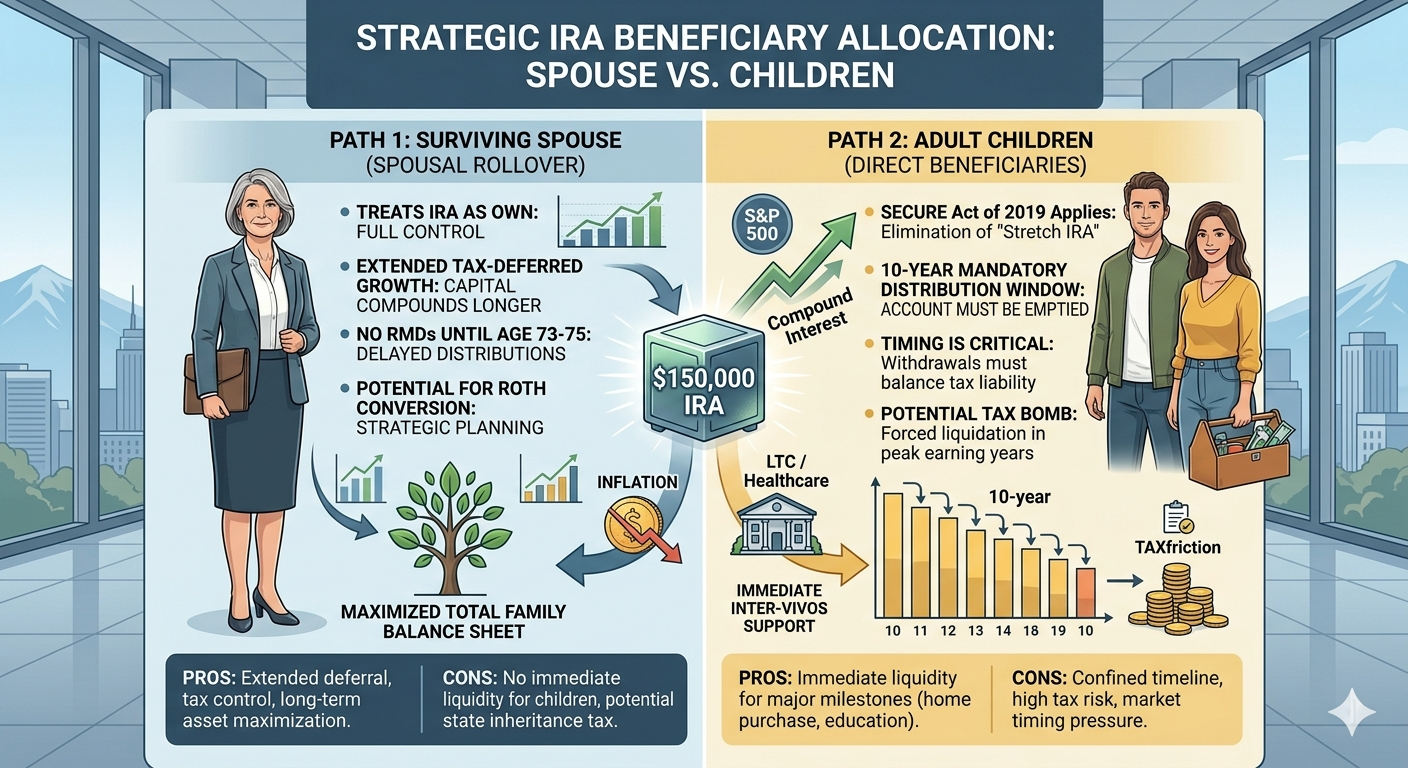

The decision to bypass a surviving spouse as the primary beneficiary of an Individual Retirement Account (IRA) in favor of adult children represents a significant shift in contemporary estate planning, particularly within the context of the “Great Wealth Transfer.” As an estimated $84 trillion is projected to pass down to younger generations over the next two decades, the strategic allocation of even modest accounts, such as a $150,000 IRA, requires a sophisticated understanding of tax law and macroeconomic trends. When a spouse possesses sufficient Social Security and independent retirement assets to maintain their standard of living, the move to name children as direct beneficiaries is often driven by a desire to optimize the terminal value of the estate. However, this maneuver is no longer as straightforward as it once was, primarily due to shifting legislative frameworks that govern how non-spouse beneficiaries must handle inherited qualified accounts.

Central to this analytical framework is the SECURE Act of 2019 and its subsequent iterations, which effectively eliminated the “stretch IRA” for most non-spouse beneficiaries. Under these current regulations, children who inherit an IRA are generally required to fully distribute the account’s assets within ten years of the original owner’s death. This creates a compressed timeline that can lead to a significant “tax bomb” if the children are currently in their peak earning years. From an economic perspective, the forced liquidation of $150,000—plus any market growth—over a decade could potentially push the beneficiaries into higher federal and state income tax brackets. This necessitates a careful calculation of the effective tax rate applied to the inheritance versus the tax rate that would apply if the spouse rolled the IRA into their own account and took distributions more slowly over a longer horizon.

The performance of the S&P 500 and broader equity markets also plays a critical role in determining the efficacy of this beneficiary strategy. If the $150,000 IRA is aggressively invested in diversified equities, the potential for compounding growth over the ten-year mandatory distribution window is substantial. Historically, the S&P 500 has provided an annualized return of approximately 10% before inflation. In a scenario where the market performs in line with historical averages, a $150,000 balance could nearly double within the ten-year period, assuming no distributions are taken until the final year. However, the requirement to empty the account means the children must time their withdrawals to balance market volatility against their personal tax liabilities, a task that becomes increasingly complex during periods of high market fluctuation or economic downturns.

Inflation remains a persistent variable that complicates the “sufficient income” calculus for the surviving spouse. While the spouse may currently feel they have enough to see them through their lifetime, the erosion of purchasing power over a 20-to-30-year retirement can be profound. Even at the Federal Reserve’s target inflation rate of 2%, the cost of living doubles roughly every 36 years; if inflation averages closer to 3% or 4%, that timeline accelerates significantly. By naming children as beneficiaries, the household is essentially betting that the spouse’s existing portfolio—likely indexed to inflation through Social Security or specific Treasury Inflation-Protected Securities (TIPS)—will remain robust enough to cover late-life healthcare costs, which often outpace general consumer price index (CPI) growth.

Interest rate environments further dictate the optimal management of these inherited assets. When interest rates are elevated, as seen in the Federal Reserve’s recent tightening cycles to combat post-pandemic inflation, fixed-income yields within an IRA become more attractive. If the IRA is heavily weighted toward bonds or money market instruments, the predictable income stream can be a boon for beneficiaries. Conversely, in a low-rate environment, the opportunity cost of holding the IRA in conservative assets increases. For children who may be using the inheritance to pay down high-interest debt, such as mortgages or student loans, the “real” value of the $150,000 is measured by the interest expenses they avoid, making the direct inheritance a powerful tool for improving their net worth and household liquidity.

The comparative advantage of a spousal rollover cannot be ignored when analyzing the total economic impact on the family unit. If the wife were to inherit the IRA, she could treat it as her own, delaying Required Minimum Distributions (RMDs) until age 73 or 75, depending on her birth year. This allows the capital to remain in a tax-deferred environment for much longer than the 10-year limit imposed on children. By extending the tax-advantaged growth period, the total nominal value of the account could end up being significantly larger when it eventually passes to the children through the wife’s estate. This creates a classic trade-off between immediate liquidity for the next generation and the long-term maximization of the total family balance sheet through extended tax deferral.

Fiscal policy and the future of the Tax Cuts and Jobs Act (TCJA) also loom large over this decision. Many of the current lower tax brackets are set to sunset at the end of 2025 unless Congress takes legislative action. If tax rates rise in 2026, children who inherit an IRA now and begin taking distributions will be doing so in a more expensive fiscal environment. An analyst must consider whether it is more efficient for the spouse to take the IRA now, potentially perform strategic Roth conversions at current lower rates, and then leave a tax-free Roth IRA to the children. This would bypass the 10-year tax liability issue entirely, providing the children with a high-value asset that does not increase their taxable income, regardless of their professional earnings.

From a behavioral economics standpoint, naming children as beneficiaries serves as a proactive form of wealth distribution that can facilitate major life milestones, such as purchasing a home or funding a grandchild’s education. In a housing market characterized by high prices and fluctuating mortgage rates, an influx of $150,000 can provide the necessary equity to secure a lower loan-to-value ratio, effectively reducing the children’s long-term financial stress. This “inter-vivos” style of thinking—distributing wealth when it is most useful rather than at the end of the second spouse’s life—is becoming increasingly popular among affluent families who prioritize the financial stability of their heirs over the absolute maximization of the estate’s size.

The role of healthcare and long-term care (LTC) costs is the most volatile factor in this economic equation. The Department of Health and Human Services estimates that 70% of adults 65 and older will need some form of long-term care. Even with a “modest” IRA of $150,000, those funds could represent a vital reserve for private-pay nursing care, which can easily exceed $100,000 per year in many jurisdictions. By diverting this asset to the children, the spouse is effectively reducing their own “margin of safety.” While Social Security and other income may cover daily expenses, they rarely cover the intensive costs of memory care or around-the-clock nursing without significantly depleting other principal assets.

Market liquidity and the composition of the children’s own portfolios should also be assessed. If the children are already high-net-worth individuals with substantial exposure to the S&P 500, receiving an additional $150,000 in a traditional IRA may simply create an unwanted tax administrative burden. However, for children who are under-saved for retirement, this inheritance functions as a critical catch-up mechanism. The economic utility of the $150,000 is therefore subjective, based on the marginal utility of wealth for each beneficiary. For a child struggling with inflation-driven increases in the cost of living, the inheritance provides immediate relief; for a wealthy child, it is merely a tax-planning challenge.

The legal structure of the IRA beneficiary designation also interacts with state-level estate and inheritance taxes. While federal estate tax exemptions are currently high—over $13 million per individual—some states have much lower thresholds or specific inheritance taxes that apply to transfers to non-spouse heirs. An analytical review of the geographic location of both the parents and the children is necessary to ensure that the $150,000 is not unnecessarily eroded by state-level levies that could have been avoided through a spousal transfer. This layer of “tax friction” can often be the deciding factor in whether a direct-to-children designation is truly the most efficient path forward.

Ultimately, the decision to name children as beneficiaries on a husband’s IRA when the wife is financially secure is a sophisticated balancing act between immediate family needs and long-term tax optimization. In an era of volatile interest rates, persistent inflation, and evolving tax codes, the move reflects a shift toward generational support. As long as the surviving spouse’s “lifetime” income is truly insulated from market shocks and catastrophic health events, using the IRA as a legacy vehicle can empower the next generation. However, this strategy requires the beneficiaries to be disciplined in their withdrawal strategies to mitigate the impact of the 10-year rule, ensuring that the federal government does not become the unintended primary beneficiary of the husband’s legacy.